Your Tax Refund Is $352 Bigger This Year — The 3-Move Plan to Make It Actually Last

The average 2026 tax refund is $3,623 — up $352 from last year. That's real money. But JPMorgan Chase Institute data shows spending spikes 119% the day a refund lands, and most of it evaporates within three months. This post breaks down a simple 3-move framework, backed by federal data, that turns your refund into more than $5,200 in first-year financial value.

TL;DR

- Average 2026 refund: $3,623 — up 10.8% from 2025 (IRS data, March 2026)

- Without a plan: 119% spending spike on day one, refund gone in roughly 3 months

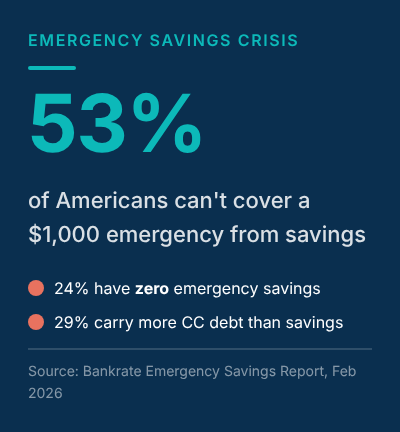

- Move 1: Set aside $500 as an emergency buffer (53% of Americans can't cover a $1,000 emergency)

- Move 2: Put $2,623 toward highest-APR credit card debt — saves $4,133 in interest at 24% APR

- Move 3: Audit subscriptions — Americans unknowingly overspend $133/month on recurring charges

- Total year-one value: $5,233+ vs. roughly $0 lasting value without a plan

Table of Contents

- Why Your 2026 Refund Is Bigger

- The Refund Disappearing Act

- Move 1: The Emergency Buffer ($500)

- Move 2: Kill Your Highest-APR Debt ($2,623)

- Move 3: Audit Your Recurring Costs

- The Full Math: 3-Move Plan vs. Do Nothing

- Frequently Asked Questions

Why Your 2026 Refund Is Bigger

The average tax refund this year is $3,623, a 10.8% jump from $3,271 in 2025. The increase comes from the OBBBA retroactive tax cuts — a larger standard deduction, boosted Child Tax Credit, and new deduction categories that went into effect for the 2025 tax year.

That extra $352 isn't a rounding error. It's 70% of a $500 starter emergency fund. The increase alone can reshape your financial safety net — if you route it intentionally before the spending impulse kicks in.

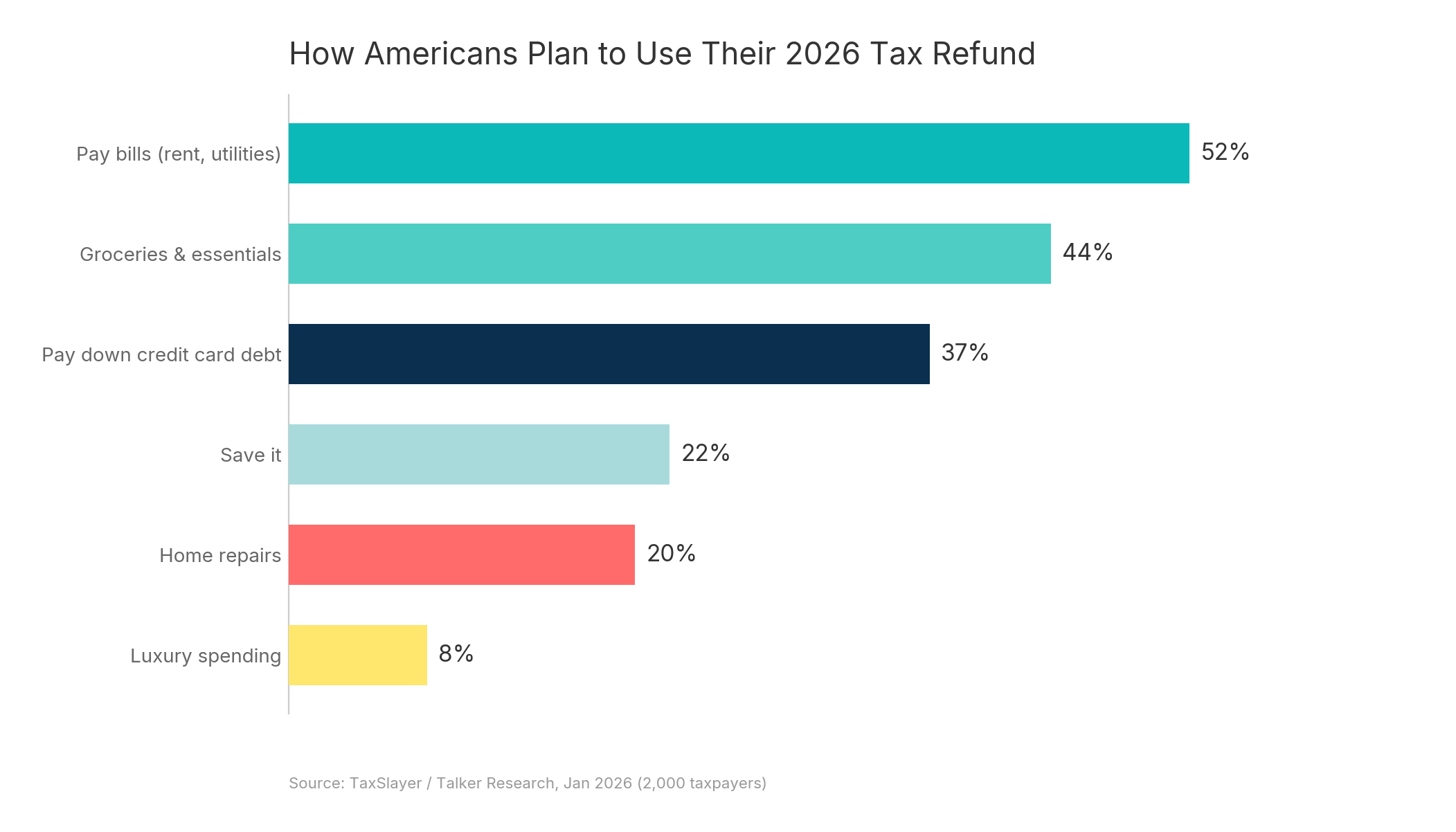

Here's what most people plan to do with their refund, according to a TaxSlayer/Talker Research survey from January 2026: 52% will pay bills, 37% will tackle credit card debt, and only 22% plan to save any of it. The instinct toward debt paydown is right. The execution — dumping it all at once without an emergency buffer — is where things go wrong.

The Refund Disappearing Act

The day your refund hits your account, spending jumps 119%. Cash withdrawals more than double. Durable goods purchases double. For 29% of recipients, refund day is the single highest cash-flow day of their entire year. This isn't speculation — it's from the JPMorgan Chase Institute's analysis of millions of actual checking accounts.

The spending timeline looks like this:

| Period | Approximate Extra Spending | Refund Remaining |

|---|---|---|

| Week 1 | ~$1,260 | $2,363 |

| Weeks 2-4 | ~$1,680 | $683 |

| Months 2-3 | ~$1,800 | $0 |

This isn't irresponsibility. It's a documented pattern that happens because refund money sits in the same checking account where daily spending happens. Without separation, it bleeds out through deferred bills, catch-up purchases, and impulse spending.

There's also a healthcare angle that rarely gets discussed. JPMorgan Chase Institute research on deferred care shows healthcare spending jumps 60% the week after a refund arrives — and 220% for the lowest-balance households. People literally postpone doctor visits until tax season. For many, this isn't bonus money. It's how they finally go to the doctor.

The good news: JPMorgan's data also shows that checking balances remain 11% above pre-refund levels six months later for people who route the money deliberately. The refund can last. It just needs a framework.

Move 1: The Emergency Buffer ($500)

The first $500 of your refund goes into a separate savings account — not your checking account. This is the move that makes the other two work.

Why $500? Because it covers the 10 most common financial emergencies: a car repair, an ER copay, an appliance failure, a surprise vet bill. According to the Bankrate Emergency Savings Report from February 2026, 53% of Americans can't cover a $1,000 emergency from savings. Twenty-four percent have zero emergency savings.

Without this buffer, the next $500 surprise goes straight onto a credit card at 20-24% APR. You pay off debt in Move 2, then a medical bill puts you right back. The buffer breaks that cycle.

The key word is separate. A savings account at a different bank, or at minimum a dedicated savings account that isn't linked to your debit card. Money in your checking account isn't saved — it's pre-spent.

Remember: your extra $352 this year already covers 70% of this buffer. The increase alone gets you most of the way to the recommended $300-500 starter emergency fund that financial experts suggest as a minimum.

Move 2: Kill Your Highest-APR Debt ($2,623)

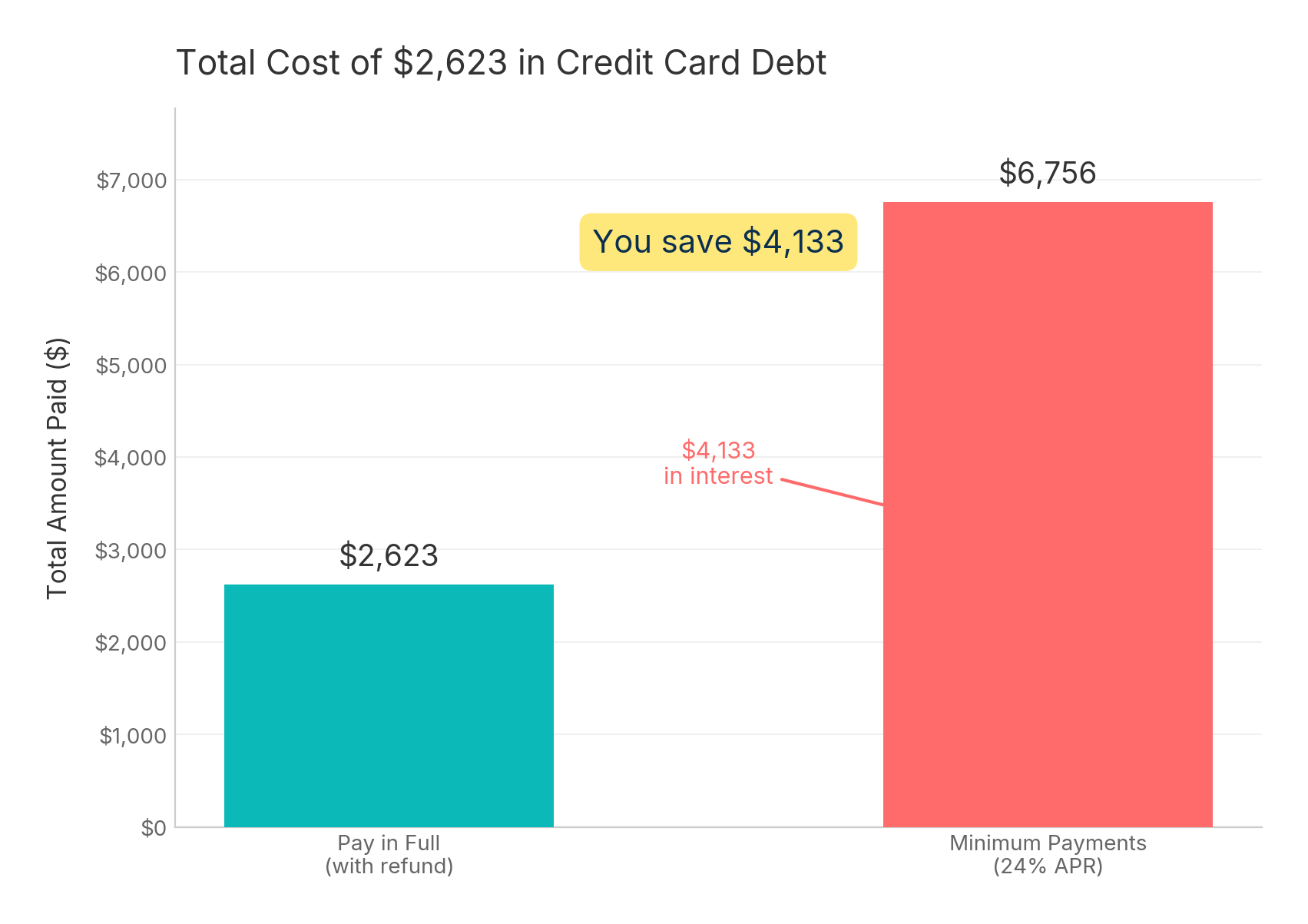

After the $500 buffer, you have $2,623 left from the average refund. All of it goes to your highest-APR credit card.

The math is striking. At 24% APR (the current average for new cards, per Federal Reserve G.19 data), $2,623 in credit card debt paid only through minimum payments takes 14.2 years to pay off and costs $4,133 in total interest. Pay it off today with your refund, and you save that entire $4,133. That's a 158% guaranteed return.

The savings scale with your APR:

| Your APR | Years to Pay Off (Minimums) | Total Interest Saved |

|---|---|---|

| 21% | 13.7 years | $3,548 |

| 24% | 14.2 years | $4,133 |

| 28% | 14.8 years | $4,925 |

Store cards and subprime cards regularly charge 28% or higher. At that rate, paying off $2,623 now saves nearly $5,000 — almost double the original balance. No savings account, stock, or bond delivers a guaranteed return like eliminating high-interest debt.

Even if you carry more than $2,623 (the average personal credit card balance is $6,523), this payment knocks off 40% of the balance and immediately reduces monthly interest from roughly $52 to $31 at 24% APR. Every dollar of principal you eliminate stops generating interest forever.

Why Move 2 comes after Move 1: Thirty-seven percent of people plan to use their refund for credit card debt — good instinct. But without the $500 buffer from Move 1, the next emergency goes right back on the card. Buffer first, then debt kill.

Move 3: Audit Your Recurring Costs

Move 3 costs zero dollars from your refund but delivers hundreds per year in freed cash flow.

According to C+R Research, Americans think they spend $86 per month on subscriptions. The actual number is $219 per month. That $133 monthly gap — money people don't even realize they're spending — adds up to $1,596 per year.

You don't need to cancel everything. Cancel $50 per month in forgotten or barely-used subscriptions and you free up $600 per year, every year. That's recurring savings that compounds indefinitely.

Here's how to do the audit in 15 minutes:

- Pull your last 3 months of bank statements. Look for every recurring charge. Mark each one as "keep," "cancel," or "not sure."

- Check the "not sure" pile. If you haven't actively used the service in the past 30 days, cancel it. You can always re-subscribe later.

- Look for duplicates. Multiple streaming services, overlapping cloud storage, gym memberships you replaced with home workouts.

- Switch annual billing where possible. Many services offer 20-40% discounts for annual plans versus monthly.

Other recurring cost targets beyond subscriptions: insurance (switching providers saves $200-500 per year on average), phone plans (prepaid carriers are often half the price of big carriers for the same coverage), and unused memberships.

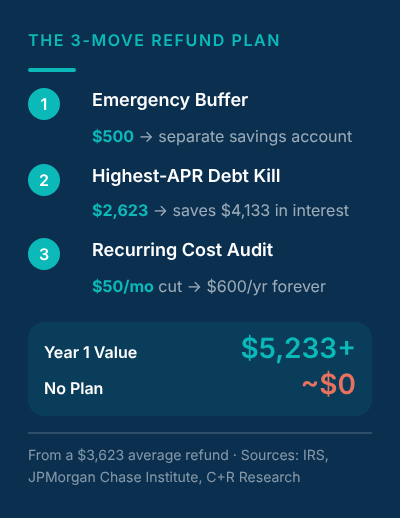

The Full Math: 3-Move Plan vs. Do Nothing

Here's the total picture when you stack all three moves together.

| Year 1 Value | Year 5 Value | |

|---|---|---|

| 3-Move Plan | $5,233+ | $7,633+ |

| No Plan | ~$0 lasting value | ~$0 plus $4,133 interest still building |

The breakdown: $500 in emergency protection, $4,133 in interest you'll never pay, and $600 per year in subscription savings. Over five years, the compounding effect of eliminated recurring costs pushes total value past $7,600.

The contrast is stark. Without a framework, your $3,623 is statistically gone within three months. With three deliberate moves — taking maybe 30 minutes total — the same money generates more than $5,200 in measurable financial value in year one alone.

Frequently Asked Questions

How much is the average tax refund in 2026?

The average 2026 tax refund is $3,623 as of March 2026, according to IRS Filing Season Statistics. That's up $352 (10.8%) from the 2025 average of $3,271. The increase is primarily driven by OBBBA retroactive tax cuts, including a larger standard deduction and boosted Child Tax Credit.

What should I do with my tax refund if I have credit card debt?

Set aside $500 as an emergency buffer first, then put the remaining amount toward your highest-APR credit card. Skipping the buffer is the most common mistake — without it, the next unexpected expense goes right back on the card. After the buffer, every dollar toward high-interest debt delivers a guaranteed return equal to your APR.

How fast do people usually spend their tax refund?

JPMorgan Chase Institute research shows spending spikes 119% on the day a refund arrives. Most refunds are effectively gone within 2-3 months without a deliberate plan. However, the same research shows balances remain 11% higher after six months for people who manage the money intentionally.

Is $500 enough for an emergency fund?

A $500 starter fund covers the 10 most common financial emergencies, including car repairs, ER copays, and appliance failures. Financial experts recommend building toward 3-6 months of expenses over time, but $500 is the critical first step — it prevents the most common scenario where a single emergency sends people back into credit card debt.

How do I find subscriptions I forgot about?

Review your last three months of bank and credit card statements for any recurring charges. Most people find $133 per month more than they expected, according to C+R Research. Cancel anything you haven't actively used in the past 30 days — you can always re-subscribe if you miss it.

Make Your Refund Work Harder Than You Did for It

Your 2026 refund is $352 bigger than last year. That's not a windfall — it's an opportunity to break the cycle where refund money disappears into the same spending patterns that created the financial pressure in the first place.

The 3-move framework works because it addresses the three biggest leaks: no emergency cushion (53% of Americans), high-interest debt compounding silently (24% APR average), and subscription creep you can't see ($133/month hidden). Thirty minutes of deliberate action now creates more than $5,200 in value this year.

The refund hits your account once. What you do in the first 48 hours determines whether it lasts 48 hours or reshapes the next 48 months.