7 Places That Give You Emergency Cash Before Payday (That Aren't Payday Lenders)

When you're short before payday and you Google "need money before payday," the first results are payday lenders charging 300–600% APR. The alternatives exist — but they don't have big marketing budgets.

Here are 7 places that can give you emergency cash before payday, with exactly what each one covers, who qualifies, and how to access it.

TL;DR

- Call or text 211 — free 24/7 referral service that connects you to local emergency assistance for utilities, rent, and more

- Credit union PALs — payday alternative loans capped at 28% APR (vs. 400% for payday loans)

- Your employer — many have formal paycheck advance programs; earned wage access apps like Payactiv may already be available

- Community Action Agencies — over 1,000 nationwide offering emergency grants (no repayment)

- Salvation Army + LIHEAP — emergency assistance for utilities and bills if you meet income guidelines

- Mutual aid networks — neighbors helping neighbors, no applications, no repayment required

Table of Contents

- Why This Matters: The Math on Payday Loans

- 1. Dial or Text 211

- 2. Credit Union Payday Alternative Loans (PALs)

- 3. Community Action Agencies

- 4. Your Employer (Paycheck Advance)

- 5. Salvation Army Emergency Assistance

- 6. LIHEAP and State Emergency Programs

- 7. Local Mutual Aid Networks

- Quick Comparison

- Frequently Asked Questions

Why This Matters: The Math on Payday Loans

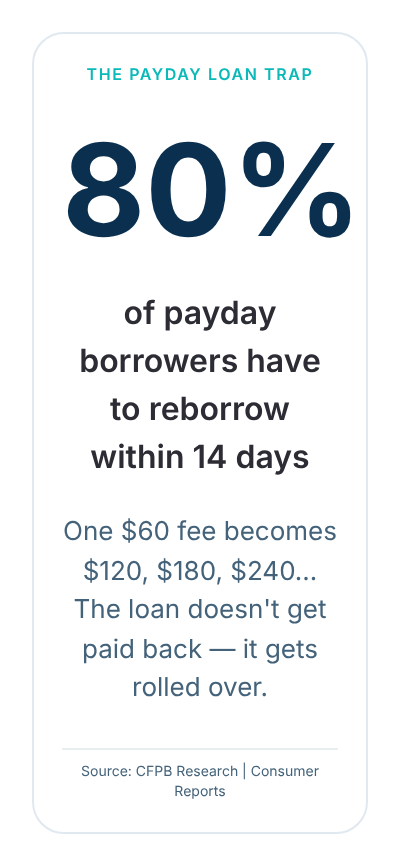

A $400 payday loan for 14 days costs $60 in fees — that's a 391% annual percentage rate (APR), according to the CFPB. In plain terms: to borrow $400 until payday, you pay $60 just for two weeks.

The problem gets worse from there.

80% of payday borrowers can't repay on the first due date and have to reborrow, according to CFPB research. That $60 fee becomes $120, then $180. The Center for Responsible Lending found payday lenders extracted $2.4 billion in fees from borrowers in a single year.

Meanwhile, 67% of Americans live paycheck to paycheck in 2025, according to Investopedia. This isn't a niche problem.

The 7 alternatives below aren't perfect for every situation — but all of them are meaningfully cheaper than a payday loan, and most people never find them because they don't show up in search.

1. Dial or Text 211

What it is: A free, confidential national helpline — call or text "211" from any phone. A trained specialist answers 24/7 and connects you to local programs for utilities, rent, food, and emergency financial assistance.

How fast: Immediate referral by phone. The actual help depends on the local program — some provide same-day assistance, others within a few days.

Who it's for: Anyone facing a financial crisis. 211 isn't just for people experiencing homelessness — it's for employed people who hit a rough week, too. No income verification required to call.

What they can actually do:

- Connect you to LIHEAP for utility bills

- Refer you to emergency rent assistance programs

- Find local food banks to free up cash for other bills

- Link you to Community Action Agencies in your area

- In some regions, connect to direct cash assistance programs

211.org made over 25 million referrals in 2025 for housing, homelessness, and utility assistance. The service is available in all 50 states.

How to use it: Call or text 211. Or go to 211.org to search by location. It's free, anonymous, and takes 10 minutes.

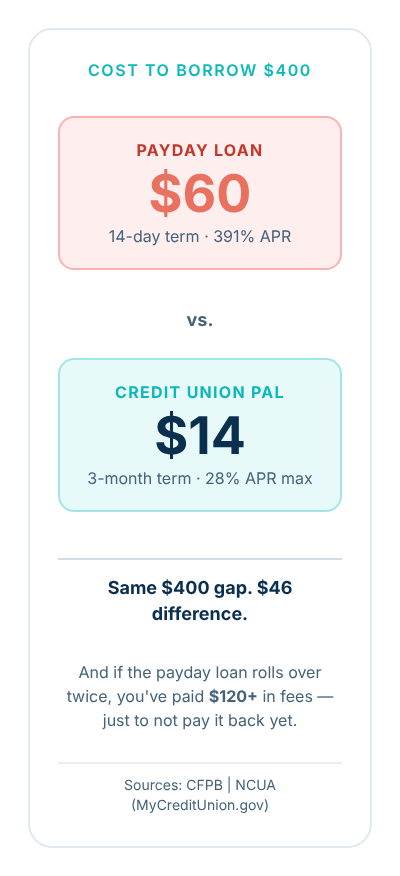

2. Credit Union Payday Alternative Loans (PALs)

What it is: Small-dollar loans offered by federal credit unions, specifically designed as payday loan alternatives. Regulated by the NCUA (National Credit Union Administration).

The numbers:

| Payday Loan | Credit Union PAL | |

|---|---|---|

| Loan amount | Up to $500 (typical) | $200–$2,000 |

| APR | 300–600% | Max 28% |

| Term | 2 weeks | 1–12 months |

| Cost on $400 | $60+ | ~$14 |

| Rollover allowed | Yes (debt trap) | No |

Two types:

- PAL I: $200–$1,000, 1–6 month term, max 28% APR

- PAL II: Up to $2,000, 1–12 month term, max 28% APR

Application fee is capped at $20. Cannot be rolled over.

How to qualify: You must be a credit union member for at least one month. Not every credit union offers PALs — search MyCreditUnion.gov to find one near you, or call NCUA at 1-800-755-1030.

How fast: Once a member, application to funds can take 1–3 business days.

The catch: You have to be a credit union member first. But many credit unions have open membership — you just need to live or work in their area.

3. Community Action Agencies

What it is: A network of approximately 1,000 nonprofit organizations across the country, funded by the federal Community Services Block Grant. They help families in or near poverty with emergency cash, rent, utilities, food, and job training.

The key difference: Some offer one-time emergency grants — not loans. You don't pay it back.

What they typically cover:

- Emergency rent or mortgage to prevent eviction

- Utility bills to prevent shutoff

- Food assistance (frees up cash for other bills)

- One-time cash grants for specific documented emergencies

Who qualifies: Generally families at or below 200% of the federal poverty level (varies by agency and available funding). That's roughly $31,000/year for a single person and $64,000 for a family of 4.

How to find one: Call 211 and ask for the Community Action Agency in your area, or search at community-action.org.

How fast: Varies. Some process requests within 2–5 business days for documented emergencies.

4. Your Employer (Paycheck Advance)

What it is: An advance on wages you've already earned, repaid via payroll deduction. Two forms: a direct HR request, or an earned wage access (EWA) app if your employer offers one.

The cost: Often free or very low fee — nothing like a payday loan.

Two paths:

HR advance: Ask your HR department for a payroll advance form. No federal law prohibits this. Many companies have formal policies — employees submit a written request, repayment is deducted from future paychecks on a schedule you agree to. This is the most underutilized option on this list.

Earned wage access (EWA): If your employer partners with DailyPay, Payactiv, EarnIn, or Tapcheck, you can access the wages you've already earned before payday.

- Payactiv: Free if you transfer to a Payactiv card with $200+ in direct deposit

- DailyPay: $1.25–$2.99 per transfer, same-day access

- EarnIn: Tip-based (no mandatory fee), up to $750 per pay period

How fast: EWA apps can fund same-day. HR advances usually take 1–3 days.

The catch: You need to be employed. Not every employer offers EWA apps. But the HR advance is available at any company — most people just don't ask.

5. Salvation Army Emergency Assistance

What it is: The Salvation Army provides emergency financial assistance for utility bills, rent, food, and prescriptions through local offices nationwide.

How it works: They typically pay your vendor or landlord directly rather than giving you cash. Your utility bill gets paid, your rent gets covered — the outcome is the same.

Who qualifies: Income limits vary by location, but most divisions serve households at or below 150–250% of the federal poverty level. You must demonstrate you have sustainable income (they're providing one-time relief, not ongoing support).

What to bring: Proof of income (pay stub or benefits statement), the bill you need help with, and valid ID. Documentation makes the process faster.

How to find your local office: Visit SalvationArmyUSA.org or call 1-800-SAL-ARMY. Appointments are available by phone at many locations.

How fast: Varies by location and available funding — typically 2–7 business days for non-crisis situations. Some offices have faster processes for utility shutoff emergencies.

6. LIHEAP and State Emergency Programs

What it is: Two different programs worth knowing:

LIHEAP (Low Income Home Energy Assistance Program) is a federal program run by states that helps with heating and cooling costs — and energy crisis situations like an imminent shutoff.

- Income limit: Up to 150% of the federal poverty level (or 60% of state median income, whichever is higher). For 2025: roughly $22,590/year for a single person, $46,800 for a family of 4.

- How to apply: Through your state's LIHEAP office or by calling 211. Some states have extended the 2025-26 application period (Pennsylvania extended theirs to May 8, 2026).

- Crisis assistance is available for households facing imminent shutoff — can be processed same-week in urgent cases.

TANF Diversion Cash Assistance is available in most states for families with children who have a short-term cash emergency but don't need ongoing assistance. It provides a one-time cash payment — available in most states, once per 12-month period.

Apply at your state's TANF office or local social services department.

How to find both: Call 211 — they know all the programs in your area and can refer you to the right one.

7. Local Mutual Aid Networks

What it is: Grassroots community networks — neighbors helping neighbors directly. No income verification, no formal application process, no repayment.

What makes them different: Every other option on this list has some eligibility bar. Mutual aid doesn't. These are community members helping community members, often through direct cash transfers via Venmo, CashApp, or PayPal.

How to find one:

- MutualAidHub.org — searchable map of networks by ZIP code

- Search "[your city] mutual aid" on Facebook, Nextdoor, or Reddit

- Reddit: r/mutualaid

How fast: Often 24–48 hours, sometimes faster. Response time depends entirely on who's active in your local network.

Reality check: Mutual aid networks run on volunteer time and donated funds. They can't help everyone, and availability varies dramatically by location. But they're worth a few minutes to check, especially if you don't qualify for formal programs.

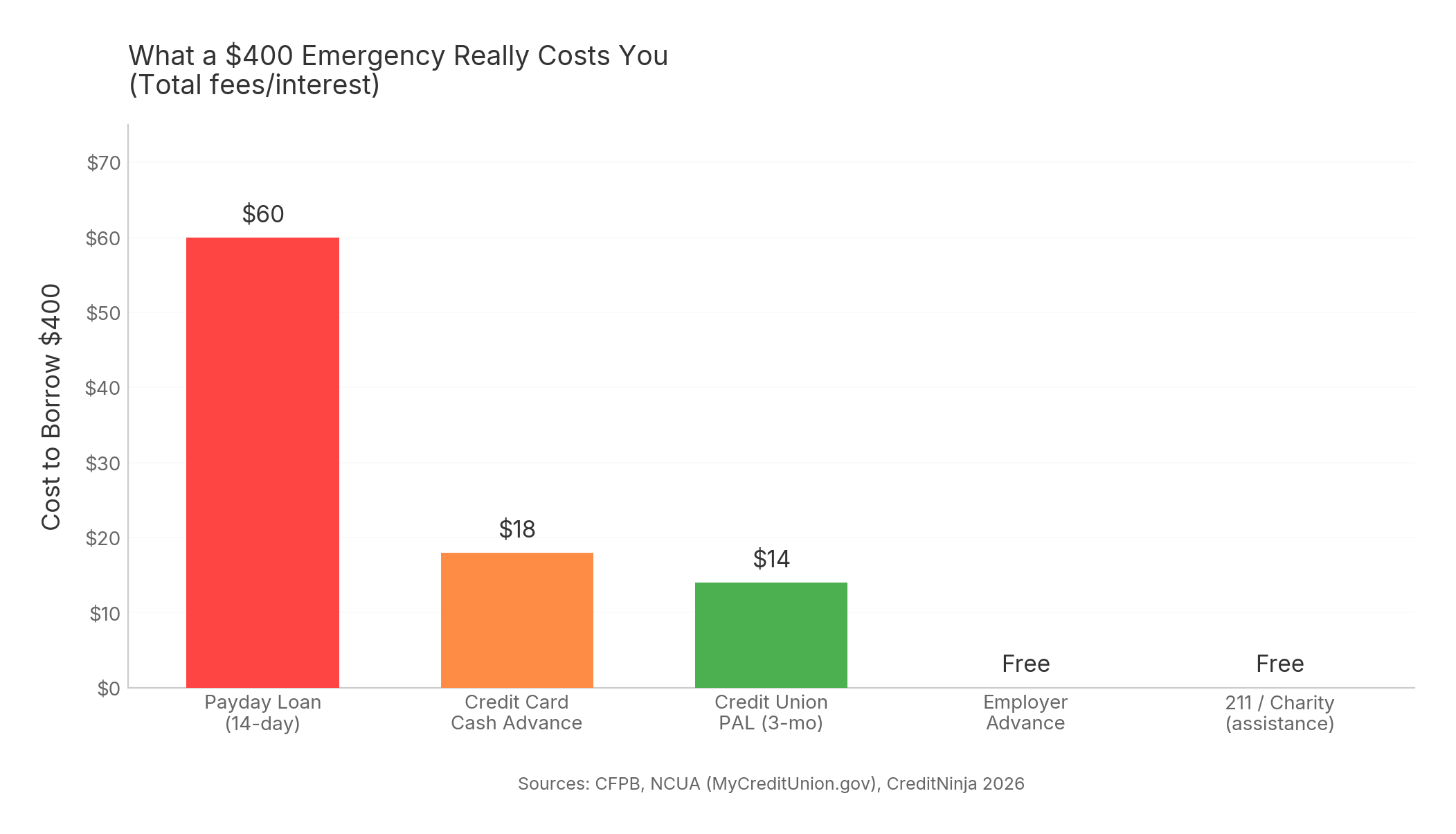

Quick Comparison

The chart above shows what borrowing $400 actually costs across different options. The payday loan is 14 days; the credit union PAL is 3 months — and still costs less. Employer advances and community resources cost nothing at all.

| Option | Speed | Cost | Who Qualifies |

|---|---|---|---|

| Employer advance / EWA | Same day | Free–$3 | Employed people |

| Mutual aid network | 24–48 hours | Free | Anyone |

| 211 referral | Immediate | Free | Anyone |

| Community Action Agency | 2–5 days | Free (grants) | Income-qualified |

| Salvation Army | 2–7 days | Free | Income-qualified |

| LIHEAP | 3–10 days (crisis: faster) | Free | Income-qualified |

| Credit union PAL | 1–3 days | ~$14 on $400 | Credit union members |

| Payday loan | Same day | $60+ on $400 | Anyone with a paycheck |

Frequently Asked Questions

What are the best payday loan alternatives?

The best payday loan alternatives depend on your situation. For same-day access: ask your employer for a paycheck advance or use an earned wage access app. For free assistance: call 211 for referrals, contact a Community Action Agency, or find a local mutual aid network. For a small loan you pay back: credit union Payday Alternative Loans (PALs) cap out at 28% APR — compare that to 300–600% APR for payday loans.

How can I get emergency cash today without a payday loan?

For same-day emergency cash: ask your employer's HR department about a paycheck advance (many companies have formal policies), use an earned wage access app if your employer offers one, or reach out to a local mutual aid network. Dial or text 211 for immediate referrals to local resources — they can often connect you to same-day assistance for specific bills.

What is a Payday Alternative Loan (PAL)?

A PAL is a small-dollar loan offered by federal credit unions, regulated by the NCUA. PAL I loans are $200–$1,000 with a max 28% APR and 1–6 month repayment terms. PAL II goes up to $2,000 over 1–12 months. Application fee is capped at $20. To qualify, you must be a credit union member for at least one month. Find a credit union near you at MyCreditUnion.gov.

Does 211 give you money?

211 doesn't give money directly — it's a free, confidential referral service that connects you to local programs that do. Specialists are available 24/7 and can refer you to programs for utilities, rent, food, and emergency cash assistance based on what's available in your area. Call, text 211, or use 211.org.

What is the fastest way to get emergency cash before payday?

The fastest options: an employer paycheck advance or earned wage access app (same day), a local mutual aid network (24–48 hours), or calling 211 for referrals to programs with crisis same-week processing. For bills specifically (utility shutoff, overdue rent), LIHEAP and local Community Action Agencies can sometimes act quickly for documented emergencies.

A Note on Breathing Room

The 7 options above exist before any app or product enters the picture. A real emergency is a real emergency — these are the resources most people never find.

For the recurring situation — the week before payday when cash is tight but not crisis-level — that's exactly what Cash Flex™ is for. Eligible Panda Pay users can access up to $100 in temporary cash flow support with no interest and no late fees. It's not a loan. It's a bridge.

But first — the free resources. They exist for a reason.